3rd February 2022

Coronavirus Pandemic - Is the End in Sight?

Remarkably, we are now into our third calendar year of the COVID-19 coronavirus crisis. No sooner did we think the worst of the pandemic was behind us, when the WHO moved even further along the Greek alphabet and declared that the “Omicron” variant was upon us, potentially the most dangerous one yet. As it turns out, Omicron proved to be much more infectious than earlier strains of the virus, but generally less deadly. It has been a stark reminder though, that the pandemic is not over with yet.

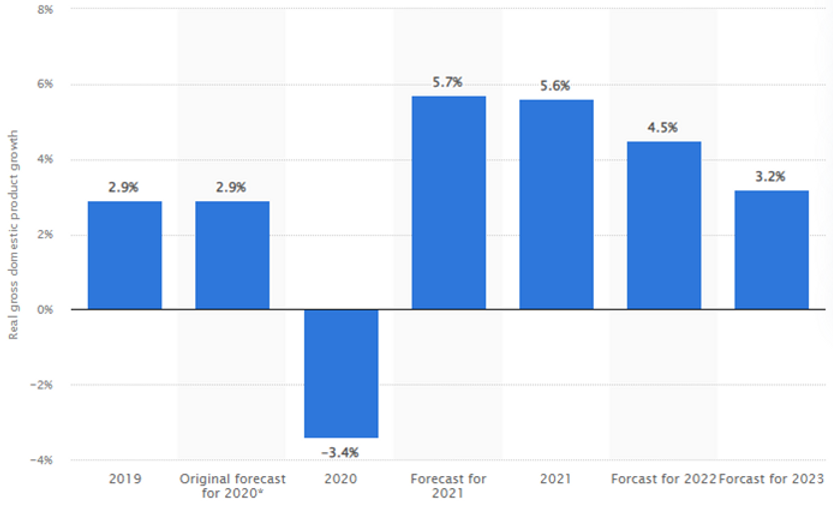

The impact on the global economy of the pandemic is truly unprecedented. Most of the world tumbled into recession, with economies more reliant on services (such as the UK) being hit hardest. Supply chains dried up (and are still struggling to recover), unemployment soared, and government debt reached obscene levels as governments pumped money into their economies to keep them afloat. The below graph shows the impact on global gross domestic product (GDP) and the predicted outcomes for this year and next.

Early estimates from economists predicted that, should the virus become a global pandemic, most major economies would experience a loss of at least 2.9 percent of their GDP over 2020. This forecast was already restated to a GDP loss of 3.4 percent. To put this number in perspective, global GDP was estimated at around 84.54 trillion U.S. dollars in 2020 – meaning that a 4.5 percent drop in economic growth results in almost 2.96 trillion U.S. dollars of lost economic output. Almost an unbelievable figure.

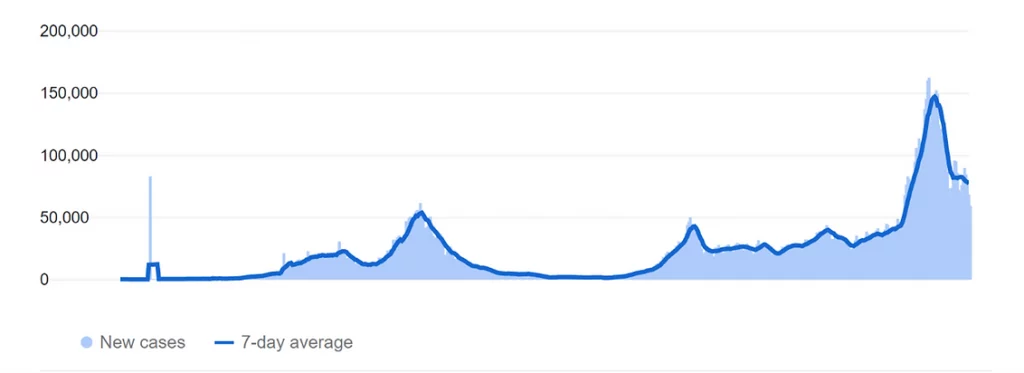

The economic impact is of course only one aspect of the pandemic, with health being the most in-focus. The below graph shows the three waves of infections in the UK. The more recent spike cause by the omicron variant was by far the most severe, but thanks to a strong vaccination programme, hospitalisations and death rates are much reduced from the prior two waves of infections. Around the world we have observed largely the same pattern as below (UK).

Globally, 376 million people have been infected, over 5.5 million have died, and nearly 10 billion doses of vaccines have been administered. Despite obvious setbacks, there has been major progress in defeating the virus to date. Whilst some countries remain in heavy economic restrictions, such as Australia, others have loosened measures and are beginning to return to semblances of normality. The UK have taken this a step further still and ended nearly all coronavirus restrictions – with the exception of quarantine for those who test positive – and set about life post-Covid.

In the UK, a remarkable 91% of the population has received at least their first dose of the vaccine, with nearly two-thirds having had both shots and a booster (three jabs) since the vaccination rollout began. Vaccination rates in the developed world have been exceptional. However, there is a different story in emerging economies, which have struggled to purchase and distribute vaccines fast enough to counter the spread. Many have been relying on donations from more developed nations, but unfortunately this number fell far below what was pledged. The saying “no-one is safe until everyone is safe” rings true here, in that, until the whole world is protected against the virus, it will continue to mutate and present potentially dangerous variants that could be more harmful to those who are unvaccinated. The hope that this pandemic can become an epidemic can only be reached once most of the world can learn to live with the virus.

We must remain cautious, though. From the outset of the pandemic, many well-respected experts have consistently gotten their predictions wrong. Risks remain high, with new variants being discovered that are more able to overcome the effects of vaccines. It may be too early to declare the end of the pandemic, but we are cautiously optimistic that the worst is now behind us.

Disclaimer:

The opinions expressed in this update are those of A&J Wealth Management Limited only, as at 3rd February 2022, and are subject to change.

The content of this publication is for information purposes and should not be treated as a forecast, research or advice to buy or sell any particular investment or to adopt any investment strategy. It does not provide personal advice based on an assessment of your own circumstances. Any views expressed are based on information received from a variety of sources which we believe to be reliable but are not guaranteed as to accuracy or completeness. Any expressions of opinion are subject to change without notice.

The tax treatment depends on your individual circumstances and may be subject to change in future.

Past performance is not a reliable indicator of future results. Investing involves risk and the value of investments, and the income from them, may fall as well as rise and are not guaranteed. Investors may not get back the original amount invested.

In addition to statements provided by A&J, you will receive regular account valuations from your product provider which should be read in conjunction with our reports and will include further details such as fees and transactions. You will also receive information about your plan annually with itemised charges. A more detailed breakdown of fees can be provided upon request, where relevant.